MCA Factor Rate Explained: What It Is, How to Calculate It, and What It Means for Merchants

May 1, 2026 · MCA Broker Stack

The factor rate is the most misunderstood cost metric in merchant cash advance, and the most frequently used by merchants — and sometimes even brokers — to compare deals incorrectly. As an MCA broker, your ability to explain the factor rate accurately, calculate its true cost, and help merchants understand what they are actually paying is one of the most important skills in your toolkit.

What Is a Factor Rate?

A factor rate is a decimal multiplier applied to the advance amount to determine the total repayment obligation. Factor rates typically range from 1.15 to 1.49 in the current market, with most standard deals falling between 1.20 and 1.40.

- 1.15 factor rate = merchant repays $1.15 for every $1.00 received

- 1.30 factor rate = merchant repays $1.30 for every $1.00 received

- 1.49 factor rate = merchant repays $1.49 for every $1.00 received

Total Repayment = Advance Amount × Factor Rate Cost of Capital = Total Repayment − Advance Amount

Factor Rate Calculation: Three Real Examples

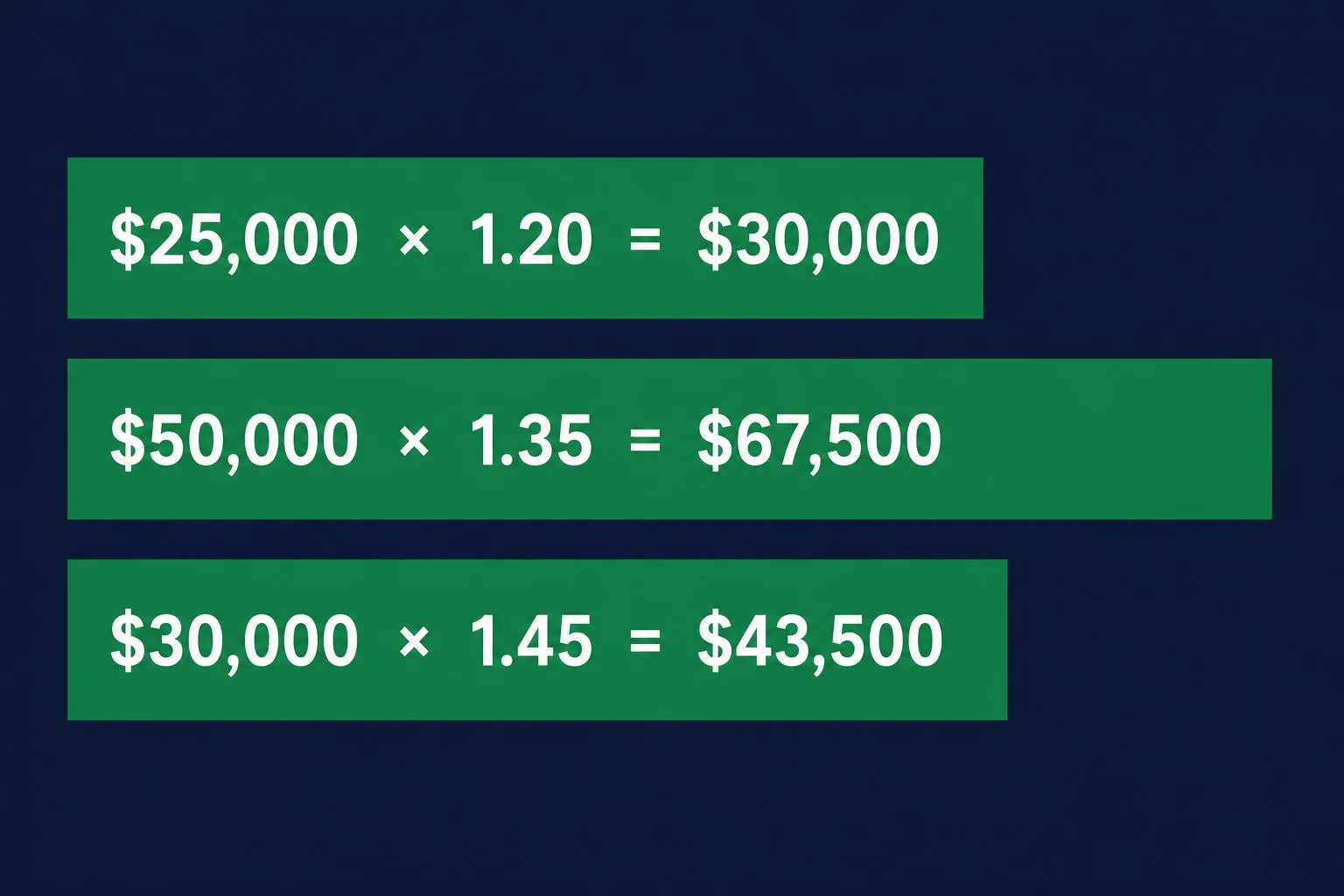

Example 1: Strong Profile

- Advance: $25,000 | Factor Rate: 1.20

- Total Repayment: $30,000 | Cost of Capital: $5,000

Example 2: Mid-Tier Deal

- Advance: $50,000 | Factor Rate: 1.35

- Total Repayment: $67,500 | Cost of Capital: $17,500

Example 3: Higher-Risk Profile

- Advance: $30,000 | Factor Rate: 1.45

- Total Repayment: $43,500 | Cost of Capital: $13,500

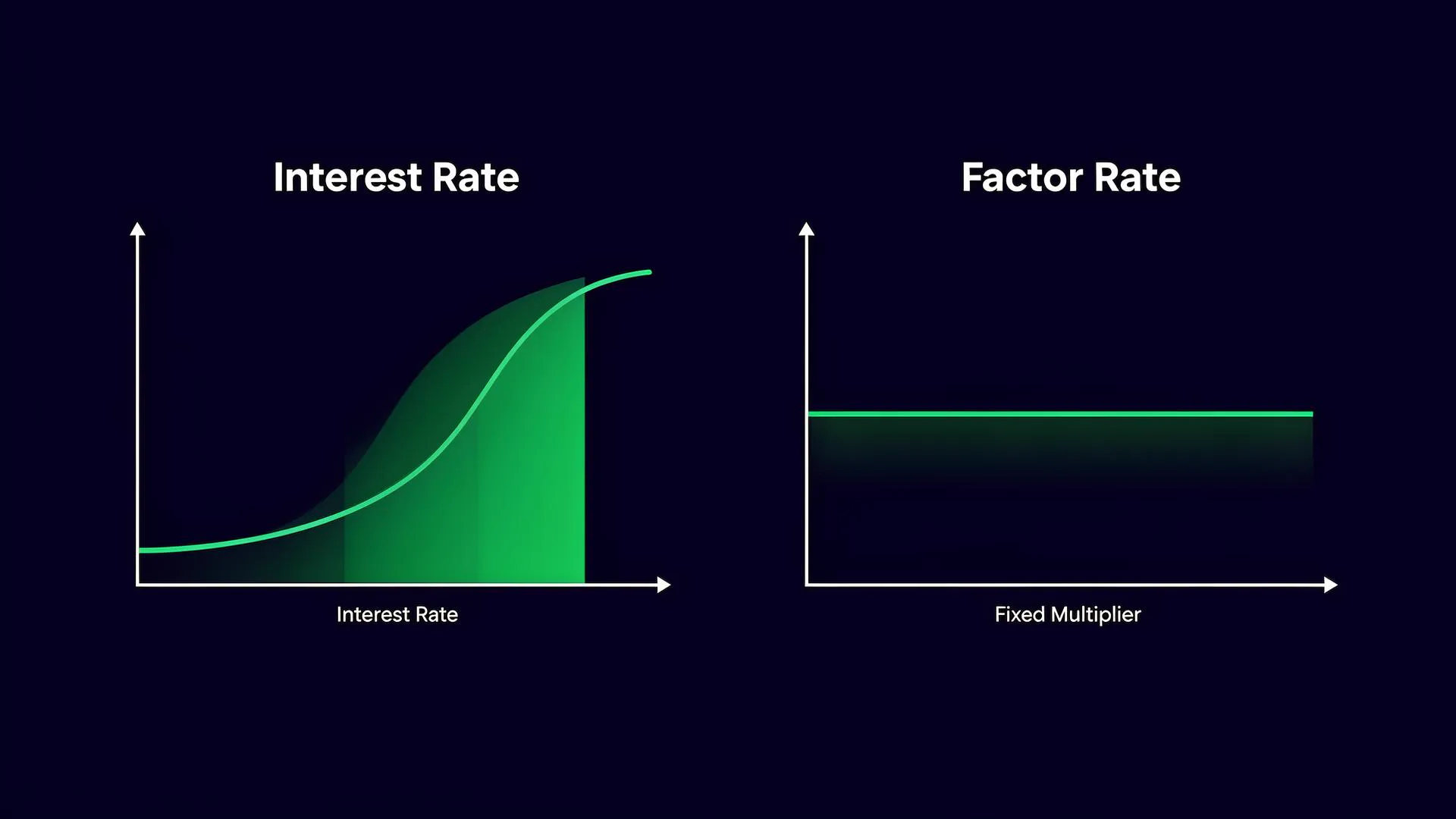

Factor Rate vs. Interest Rate: The Key Differences

| Feature | Interest Rate (Loans) | Factor Rate (MCA) |

|---|---|---|

| Type | Percentage per time period | Flat decimal multiplier |

| Cost of early repayment | Decreases (less interest accrues) | No change — fixed at origination |

| Calculation basis | Outstanding principal balance | Original advance amount only |

| Compounding | Yes | No |

The most important practical difference: with a factor rate, paying off your advance early does NOT reduce the total amount owed. The repayment amount is fixed at origination. Some funders offer an early payoff discount — always ask, but never assume it is automatic.

How to Convert a Factor Rate to an Effective APR

Effective APR = (Cost of Capital ÷ Advance Amount) ÷ Repayment Term in Years × 100

Using a $50,000 advance at 1.30 factor rate with a 9-month repayment term:

- Cost of capital: $15,000

- Effective APR: ($15,000 ÷ $50,000) ÷ 0.75 × 100 = 40% APR

The same advance repaid in 6 months = 60% APR — same total cost, higher APR because of shorter time. This is why APR is an incomplete metric for MCAs.

What Determines the Factor Rate a Merchant Receives?

Factors That Lower the Rate (Favorable)

- High and consistent average monthly deposits

- High average daily balance

- Low or zero NSF/returned items

- Long time in business (3+ years)

- No existing MCA positions

- Good personal credit (650+)

- Low-risk industry (restaurants, retail)

Factors That Raise the Rate (Unfavorable)

- Inconsistent or declining revenue

- Low average daily balance

- Multiple NSFs per month

- Short time in business (under 12 months)

- Existing MCA positions

- Recent judgments, liens, or bankruptcies

- High-risk industry (construction, trucking)

For a complete breakdown of the underwriting signals funders weigh, see our guide on MCA underwriting criteria.

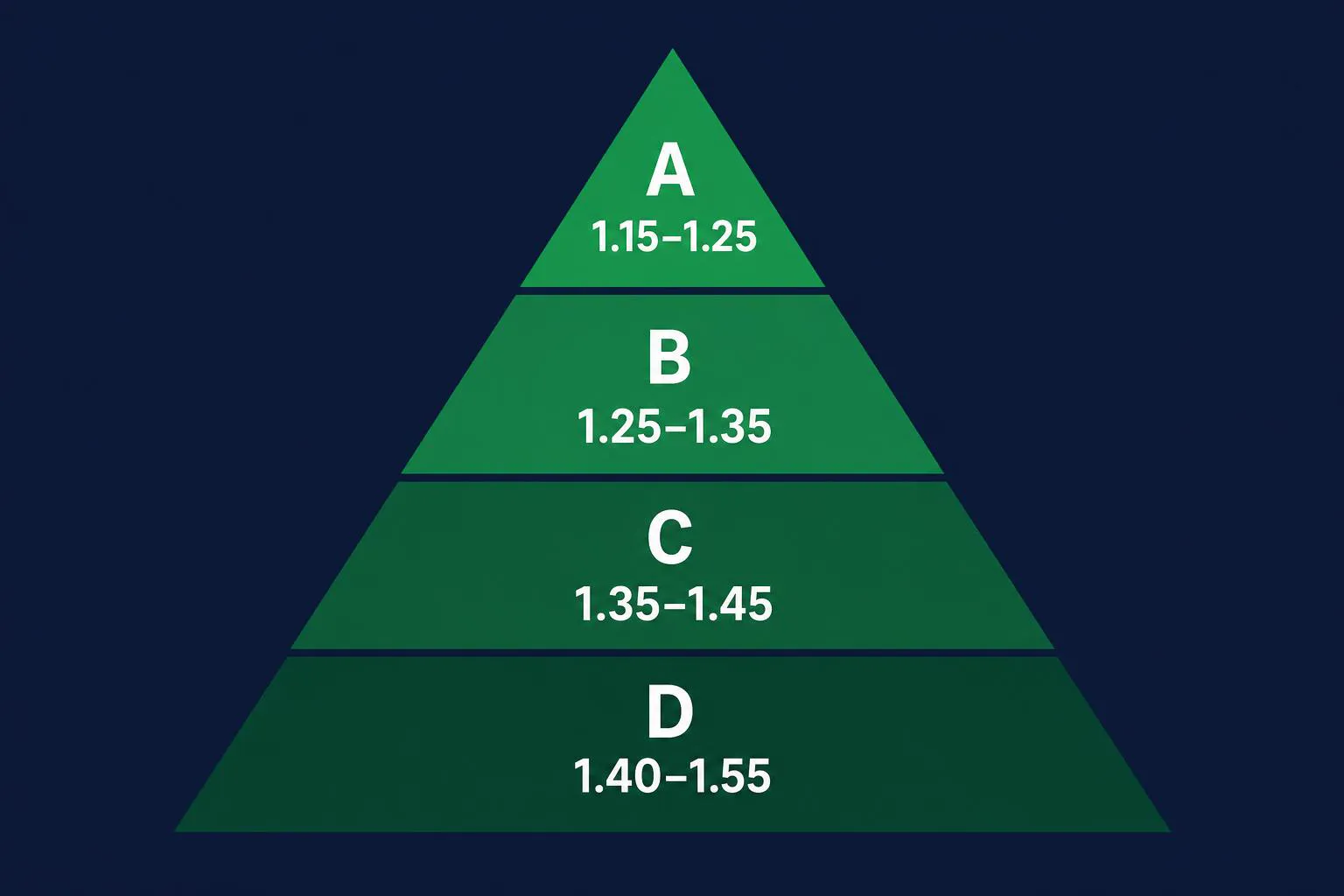

Factor Rates by Deal Tier

| Credit Tier | Profile | Typical Rate Range |

|---|---|---|

| A Paper | Strong revenue, excellent bank health, 2+ years, 650+ FICO | 1.15–1.25 |

| B Paper | Solid revenue, minor NSFs, 1–2 years, 580–649 FICO | 1.25–1.35 |

| C Paper | Moderate revenue, some NSFs, one existing MCA | 1.35–1.45 |

| D Paper | Lower revenue, higher NSFs, 2nd position | 1.40–1.55 |

How to Explain Factor Rates to Merchants

Step 1: Lead with total cost "On this advance of $50,000, the total you will repay is $67,500. The cost to access this capital is $17,500."

Step 2: Contextualize with the daily payment "Based on your monthly revenue, the daily payment comes to approximately $750 each business day."

Step 3: Explain the timeline "At your current revenue, we estimate this pays off in approximately 7–8 months."

Step 4: Address the factor rate question directly if raised "The factor rate of 1.35 is the multiplier that determines your total repayment. It's not an interest rate — the cost doesn't grow over time. It's a fixed fee agreed to upfront."

For more on guiding merchants from offer to signed contract, see how to close MCA deals.

Frequently Asked Questions

Is a lower factor rate always better?

A lower factor rate means lower total cost for the merchant. Always work to find the most competitive offer for your merchant's profile.

Does paying off the advance early reduce the factor rate cost?

No. Factor rate costs are fixed at origination. Some funders offer early payoff discounts on a case-by-case basis — always ask.

How do I know if a factor rate offer is competitive?

Submit the same merchant file to 2–3 funders simultaneously and compare offers across factor rate, holdback percentage, and funded amount.

What is the difference between factor rate and APR?

APR accounts for time; factor rate is a flat multiplier with no time component. A 1.30 factor rate on a 6-month MCA converts to approximately 60% effective APR; on a 12-month MCA, approximately 30% APR.

Published by MCA Broker Stack — the industry resource for MCA brokers and ISOs.